Maharashtra government has approved a plan to set up a task force to prepare an action plan against a recent change in the law that has brought cooperative banks under the supervision of the Reserve Bank of India (RBI).

What are Cooperative Banks?

Co-operative banks are financial entities established on a cooperative basis and belonging to their members.

This means that the customers of a cooperative bank are also its owners.

These banks provide a wide range of regular banking and financial services. However, there are some points where they differ from other banks.

They came into being with the aim to promote saving and investment habits among people, especially in rural parts of the country.

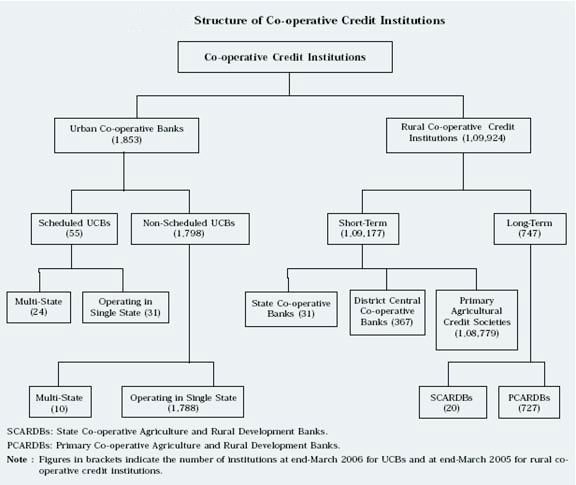

Structure of co-operative banks in India

Broadly, cooperative banks in India are divided into two categories – urban and rural.

Rural cooperative credit institutions could either be short-term or long-term in nature.

Further, short-term cooperative credit institutions are further sub-divided into State Co-operative Banks, District Central Co-operative Banks, Primary Agricultural Credit Societies.

Meanwhile, the long-term institutions are either State Cooperative Agriculture and Rural Development Banks (SCARDBs) or Primary Cooperative Agriculture and Rural Development Banks (PCARDBs).

On the other hand, Urban Co-operative Banks (UBBs) are either scheduled or non-scheduled.

Who oversees these banks?

In India, cooperative banks are registered under the States Cooperative Societies Act.

They also come under the regulatory ambit of the Reserve Bank of India (RBI) under two laws, namely, the Banking Regulations Act, 1949, and the Banking Laws (Co-operative Societies) Act, 1955.

They were brought under the RBI’s watch in 1966, a move that brought the problem of dual regulation along with it.

Features of Cooperative Banks:

Customer Owned Entities: Co-operative bank members are both customer and owner of the bank.

Democratic Member Control:Co-operative banks are owned and controlled by the members, who democratically elect a board of directors. Members usually have equal voting rights, according to the cooperative principle of “one person, one vote”.

Profit Allocation: A significant part of the yearly profit, benefits or surplus is usually allocated to constitute reserves and a part of this profit can also be distributed to the co-operative members, with legal and statutory limitations.

Financial Inclusion:They have played a significant role in the financial inclusion of unbanked rural masses.

Structure of Cooperative Banking:

Advantage of Cooperative Banking

Cooperative Banking provides effective alternative to the traditional defective credit system of the village money lender.

It provides cheap credit to masses in rural areas.

Cooperative Banks have discouraged unproductive borrowing personal consumption and have established the culture of productive borrowing.

Cooperative credit movement has encouraged saving and investment, instead of hoarding money the rural people tend to deposit their savings in the cooperative or other banking institutions.

Cooperative societies have also greatly helped in the introduction of better agricultural methods. Cooperative credit is available for purchasing improved seeds, chemical fertilizers, modern implements, etc

Cooperatives Banks offers higher interest rate on deposits.

Problems with Cooperative Banking in India

Organisational and financial limitations of the primary credit societies considerably reduce their ability to provide adequate credit to the rural population.

Needs of tenants and small farmers are not fully met.

Primary credit societies are financially weak and are unable to meet the production-oriented credit needs

Overdues are increasing alarmingly at all levels.

Primary credit societies have not been able to provide adequate and timely credit to the borrowing farmers.

The cooperatives have resource constraints as their owned funds hardly make a sizeable portfolio of the working capital. Raising working capital has been a major hurdle in their effective functioning.

A serious problem of the cooperative credit is the overdue loans of the cooperative banks which have been continuously increasing over the years.

Large amounts of overdues restrict the recycling of the funds and adversely affect the lending and borrowing capacity of the cooperative.

Most of the benefits from the cooperatives have been covered by the big land owners because of their strong socio-economic position.

Cooperative Banks are losing their lustre due to expansion of Scheduled Commercial Bank and adoption of technology. They are also facing stiff competition from payment banks and small-finance banks.

Long-term credit extended by them is declining.

Regional Disparities: The cooperatives in northeast states and in states like West Bengal, Bihar, Odisha are not as well developed as the ones in Maharashtra and Gujarat. There is a lot of friction due to competition between different states, this friction affects the working of cooperatives.

Political Interference: Politicians use them to increase their vote bank and usually get their representatives elected over the board of director in order to gain undue advantages.

Who oversees these banks?

In India, cooperative banks are registered under the States Cooperative Societies Act.

They also come under the regulatory ambit of the Reserve Bank of India (RBI) under two laws, namely, the Banking Regulations Act, 1949, and the Banking Laws (Co-operative Societies) Act, 1955.

They were brought under the RBI’s watch in 1966, a move that brought the problem of dual regulation along with it.

How has The Banking Regulation Act been amended?

Cooperative banks have long been under dual regulation by the state Registrar of Societies and the RBI.

As a result, these banks have escaped scrutiny despite failures and frauds.

The changes to The Banking Regulation Act approved by Parliament in September 2020, brought cooperative banks under the direct supervision of the RBI.

Changes brought

The amended law has given RBI the power to supersede the board of directors of cooperative banks after consultations with the concerned state government.

Earlier, it could issue such directions only to multi-state cooperative banks.

Also, urban cooperative banks will now be treated on a par with commercial banks.

And a cooperative bank can, with prior approval of the RBI, issue equity shares, preference shares, or special shares to its members or to any other person residing within its area of operation, by way of public issue or private placements.

It can also issue unsecured debentures or bonds with a maturity of not less than 10 years.

This essentially means non-members can become shareholders of the bank, and this will allow the RBI to merge failing banks quickly.

What triggered the need for the changes in the law?

India has some 1,540 urban cooperative banks, with a depositor base of 8.6 crore and deposits of at least Rs 5 lakh crore.

Finance Minister told Lok Sabha last year that the financial status of at least 277 urban cooperative banks was weak, and around 105 cooperative banks were unable to meet the minimum regulatory capital requirement.

According to RBI’s latest financial stability report, the gross non-performing asset ratio of urban cooperative banks deteriorated from 9.89 percent in March 2020 to 10.36 percent in September 2020.

Not only do these banks have high levels of bad loans, they also have a small capital base — something that the changes in the law have tried to address by allowing these banks to issue shares with RBI’s approval.

Political interference in staff appointments is also a problem with these banks, which has added to inefficiencies.

LIVE Online Class

LIVE Online Class