‘No MDR on digital payment to large firms’ GS: 3

‘No MDR on digital payment to large firms’

In news:

- The Union government recently said banks or system providers will not impose charges or merchant discount rate (MDR) on customers as well as merchants on digital payments made to establishments having turnover in excess of Rs. 50 crore from November 1.

Important facts:

- Amendments to this effect have been made in the Income Tax Act as well as in the Payment and Settlement Systems Act 2007.

- The new provisions “shall come into force with effect from November 1, 2019,” the Central Board of Direct Taxes (CBDT) said in a circular.

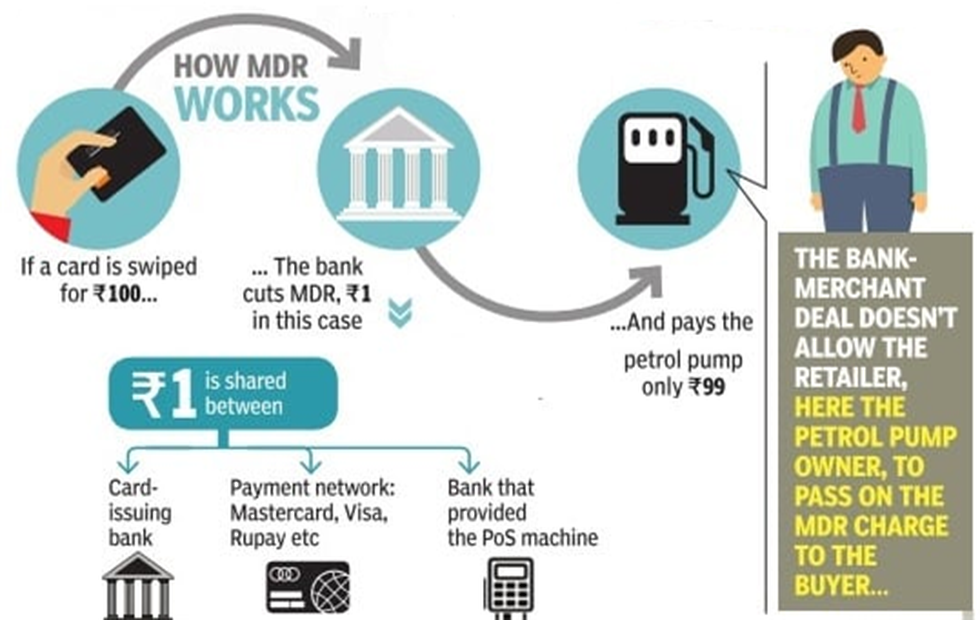

Merchant discount rate (MDR)

- MDR is charge or fee imposed on merchant by bank for accepting payment from their customers in credit and debit cards every time card is used for payments (like swiping) in their stores.

- MDR charges are usually shared in pre-agreed proportion between them and are expressed in percentage of transaction amount.

- MDR compensates bank issuing card, bank which puts up swiping machine (Point-of-Sale or PoS terminal) and network providers such as Mastercard or Visa for their services.

- In India, the RBI specifies maximum MDR charges that can be levied on every card transaction.

- Since 1 January, small merchants pay a maximum MDR of 0.4% of bill value and larger merchants pay 0.9%.

- To promote digital transactions, the government will bear MDR charges on transactions up to Rs 2,000 made through debit cards, BHIM UPI or Aadhaar-enabled payment systems.

- MDR also includes the processing charges that a payments aggregator has to pay to online or mobile wallets or indeed to banks for their service.

What was the Budget announcement?

- In her speech, Finance Minister Nirmala Sitharaman announced a slew of steps aimed at promoting digital payments and a less-cash economy.

- She pointed out that there are low-cost digital modes of payment such as BHIM UPI, UPI-QR Code, Aadhaar Pay, certain Debit cards, NEFT, RTGS etc. which can be used to promote less cash economy.

- She proposed that the business establishments with annual turnover more than 50 crore shall offer such low cost digital modes of payment to their customers and no charges or Merchant Discount Rate shall be imposed on customers as well as merchants.

- The government has mandated that neither the customers nor the merchants will have to pay the so-called Merchant Discount Rate (or MDR) while transacting digital payments.

Who will bear the MDR costs?

- If customers don’t pay and merchants don’t pay, some entity has to pay for the MDR costs.

- In her speech, the FM has said: “RBI and Banks will absorb these costs from the savings that will accrue to them on account of handling less cash as people move to these digital modes of payment.

- Necessary amendments are being made in the Income Tax Act and the Payments and Settlement Systems Act, 2007 to give effect to these provisions.“

Why are non-bank payment service providers complaining?

- Contrary to public perception, the MDR has not been made zero.

- The FM’s decision has just shifted its incidence on to the RBI and banks. However, if banks pay for the MDR it will adversely their likelihood to adopt the digital payments architecture.

- Many payments providers apprehend that the banks will find a way of passing on the costs to them. This will negatively impact the health of a sector that needs nurturing.

Payments and Settlement Systems Act, 2007:

- The Payment and Settlement Systems Act 2007, set up by the RBI, provides for the regulation and supervision of payment systems in India and designates the apex institution (RBI) as the authority for that purpose and all related matters.

- To exercise its powers and perform its functions and discharge its duties, the RBI is authorized under the Act to constitute a committee of its central board, which is known as the Board for Regulation and Supervision of Payment and Settlement Systems (BPSS).

- The Act also provides the legal basis for ‘netting’ and ‘settlement finality’.

What is a Payment System under the PSS Act 2007?

- The Section 2(1) (i) of the PSS Act 2007 defines that a payment system enables payment to be effected between a payer and a beneficiary, involving clearing, payment or settlement service or all of them, but does not include a stock exchange.

- A ‘payment system’ includes the systems enabling credit card operations, debit card operations, smart card operations, money transfer operations or similar operations.

|

Source)

https://www.thehindu.com/todays-paper/tp-business/no-mdr-on-digital-payment-to-large-firms/article29740506.ece

https://indianexpress.com/article/explained/explained-what-is-merchant-discount-rate-and-why-does-it-matter-5826776/

LIVE Online Class

LIVE Online Class